2026 IATA outlook. Revenues and profits of airlines on the rise, margins remain low

IATA forecasts that airline revenues will exceed $1.053 trillion in 2026. Profits will reach $41 billion to exceed the 2025 result, but profitability will remain low at 3.9 percent per passenger. In 2026, more than 5.2 billion people are expected to take advantage of services rendered by airlines – up 4.4 percent from today.

‘Airlines earn less from carrying one passenger than Apple makes on selling one phone case’ – said Marie Owens Thomsen, Chief Economist, IATA. Airlines currently earn $7.90 per passenger, down from a record $8.50 in 2023. However, despite persistently low margins, airlines will be better off in 2026 than they are today.

Airlines: Revenues, profits and passenger numbers on the rise

In 2026, the airline industry will generate more than $1.053 trillion in revenues – 4.5 percent more than the previous year. Carriers will earn a record $41 billion during this period ($39.5 billion in 2025), but their profitability will remain equally low at 3.9 percent per passenger.

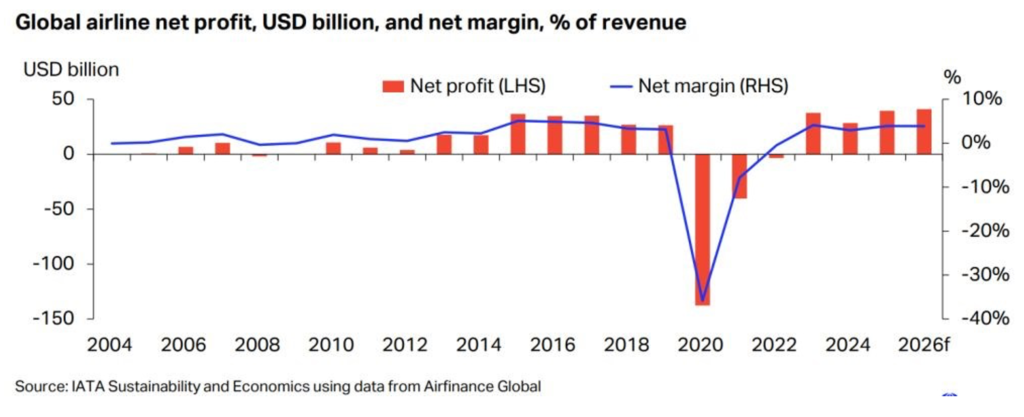

Chart: Aviation industry profits, 2004 – 2026

‘The latest forecasts show that airlines continue to exhibit remarkable resilience in the face of extremely difficult operating conditions. The carriers’ projected profits to be generated in 2026 are higher than in 2025, breaking the previous record. The net margin remains stable at 3.9 percent. The progress made is encouraging, despite remaining modest for an industry that connects global economies and provides 87 million jobs’ – stressed Willie Walsh, head of IATA.

IATA forecasts that travel demand will remain strong and expects the number of passengers to reach 5.2 billion in 2026, with a record load factor of nearly 84 percent. Changes affecting passenger travel will be accompanied by an increase in cargo traffic as well, as it is expected to reach approximately 71.6 million tons in 2026 – 2.4 percent more than today.

IATA reminds us, however, that costs remain an ever-pressing problem. Spending is rising due to labour market tensions, bottlenecks in supply chains and record high aircraft leasing rates. The situation is alleviated somewhat by persistently low fuel prices, but airlines will still have to spend more than $250 billion on fuel next year. This figure includes the planned purchases of sustainable aviation fuel (SAF) worth $4.5 billion, although supply continues to remain well below demand.

Airline revenues

As far as airline revenues are concerned, those generated on ticket sales will reach $751 billion next year – a 4.8 percent increase compared to 2025. Their growth will be driven primarily by the global increase in offering.

A growing share of non-aviation revenues will continue to be observed and is expected to reach 14 percent globally. Before the pandemic, that figure amounted to no more than 12 – 13 percent.

Cargo will account for $158 billion in revenue, a 2.1 percent increase over the previous year. This rather slow growth rate is caused primarily by global trade slowdown.

Stabilisation of costs

It is expected that in 2026, the financial situation of air carriers will be affected by fuel prices. Global spending on aviation fuel will reach $252 billion, down approximately 0.5 percent from the previous year. Unfortunately, jet fuel prices will remain high compared to oil prices, and the cost of sustainable aviation fuel (SAF) will continue to rise.

Overall, airlines will incur even higher environmental expenses next year. Costs associated with the CORSIA programme will increase to $1.7 billion – they equalled only $1.3 billion as recently as in 2025.

The cost of acquiring SAF will also grow significantly, reaching $4.5 billion, with 2.4 million tons of this type of fuel being available.

Market risks and conditions

According to IATA, persistent bottlenecks in the supply chain pose the biggest threat to airline profitability. Therefore, the process of replacing fleets will take longer than expected. Carriers must be patient and will be required to continue operating older aircraft as long as possible.

Regulatory cost pressures will play an important role as well. Increasing compliance and operational burdens will certainly adversely impact the growth of airlines. Economic uncertainty is the third risk factor. Moderate GDP growth, slowing international trade and inflation risks will also leave their mark on carriers’ finances.

However, despite operating in a difficult environment marked by supply chain problems, high labour costs and geopolitical uncertainty, airlines are showing resilience, and that is the key message. The profitability of carriers is stabilising. Nevertheless, one should not forget the industry’s continued vulnerability to crises.

Global diversification

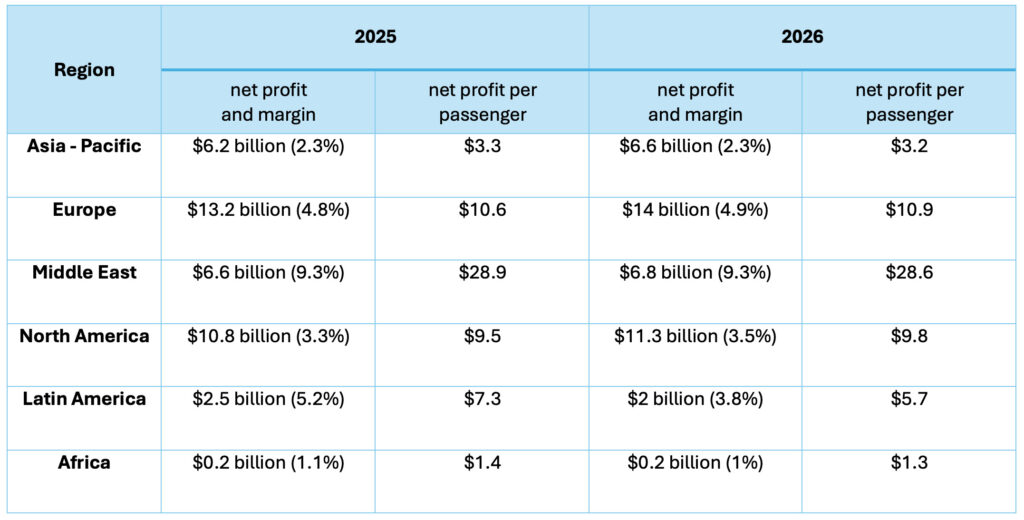

The pace at which the aviation market is growing remains, for obvious reasons, highly varied worldwide. Latin America and Africa continue to underperform when compared to other continents, and growth rates in these regions are still not high.

In the Asia-Pacific region, passenger demand remains strong, with China and India being at the very forefront of regional expansion that is driven by growing tourist activity and an expanding middle class. Easing visa requirements for those visiting China may have a positive impact on the revival of international traffic, but oversupply in this segment, observed throughout the region, remains a challenge. This particular region still remains, however, the one with the fastest growing passenger numbers and continues to be the main driver of global growth.

Interestingly, operators from Europe are expected to achieve the best financial results next year. European airlines impose a strict cost discipline and maintain high load factors thanks to efficient management practices. Low-cost carriers are doing particularly well, growing at double-digit rates and outperforming legacy airlines in terms of net profit margins, helped by strong intra-European travel rates and expansion of the leisure and tourist market. On the cost side, the strength of the euro is partially offsetting inflationary pressures, especially in connection with fuel and leasing costs. The burden posed by growing regulatory costs associated with, among other things, the ReFuelEU initiative, which requires a 2 percent share of sustainable aviation fuel (SAF) at EU airports starting in 2025, remains a tangible threat.

The Middle East remains the strongest region in terms of net profit margins and per passenger profit. This stems largely from the region’s strategic role of a global hub. Passenger demand remains high, driven by long-haul traffic and the expansion of hub carriers. However, conflicts and the tense situation in the region remain the biggest problem.

Profitability in North America remains stable, but in 2025 the region lost its position of the profitability leader to Europe. The United States has experienced stagnant overall growth and a shrinking domestic market, struggling with political uncertainty over tariffs, tighter immigration controls undermining both inbound and domestic traffic, and a prolonged government shutdown. However, 2026 should bring an increase in demand.